Struggling to save money every month? Here’s how any salaried Indian can save ₹10,000/month using simple, practical steps — no matter how small your salary is.

How to Save ₹10,000 Every Month — No Matter What Your Salary Is

Let me be honest with you for a second.

I know exactly what it feels like to get your salary credited, feel rich for about 3 days, and then suddenly wonder where all the money went before the month is even halfway done. I have been there. Most of us in India have been there.

The problem is not that you earn too little. The problem is that nobody ever taught us how to actually manage money. Not in school. Not at home. And definitely not at work.

But today, that changes.

In this post, I am going to show you exactly how to save ₹10,000 every month — whether you earn ₹20,000 or ₹1,00,000. These are not theoretical tips from a finance textbook. These are real, practical steps that actually work for salaried people in India in 2026.

Why Most Indians Struggle to Save (Be Honest With Yourself)

Before we talk about solutions, let us talk about why you are not saving right now. Because the reason matters.

Most of us fall into one of these four traps:

Trap 1 — Spend first, save whatever is left. This never works. Whatever is left at the end of the month is always zero. Always. Because life always finds a way to fill up the space.

Trap 2 — Lifestyle inflation. You got a raise last year. But somehow you are still broke. Sound familiar? Every time our income goes up, our expenses quietly go up to match it. New phone. Better restaurant. Weekend trips. Before you know it, the raise is completely invisible.

Trap 3 — No budget, just vibes. You spend based on how you feel that day. Stressed? Shopping. Bored? Swiggy. Happy? Celebrate! There is nothing wrong with enjoying life — but without a plan, you never know where the money actually went.

Trap 4 — Debt eating your salary silently. EMIs, credit card minimum payments, personal loans — if these are consuming more than 35% of your salary, saving ₹10,000 feels impossible because the math simply does not work.

Which one are you? Be honest. I was all four at different points in my life.

how to save money from salary every month India

how to save ₹10,000 every month

save money on low salary India

monthly budget planner India

50 30 20 rule India salary

how to save money in India 2026

The One Rule That Changes Everything — Pay Yourself First

Here is the single most powerful money habit I have ever learned, and it is embarrassingly simple:

Transfer your savings the moment your salary arrives. Before you pay a single bill. Before you order food. Before anything.

That is it.

Most people save what is left after spending. Rich people spend what is left after saving. That one sentence contains more financial wisdom than most MBA courses.

Set up an automatic transfer — the same day your salary hits your account — that moves ₹10,000 (or whatever your target is) into a separate savings account. Not your main account. A different one. Ideally one you cannot easily access on a whim.

When the money is gone from your main account before you can touch it, something magical happens. You automatically adjust. You find ways to make do with what is left. Because you have no other choice.

The 50-30-20 Rule — Made Simple for India

You may have heard of the 50-30-20 rule. It is a simple budgeting framework that works beautifully for Indian salaried professionals. Here is how it works:

| Category | Percentage | What Goes Here |

|---|---|---|

| Needs | 50% | Rent, groceries, EMIs, bills, transport |

| Savings | 20% | SIP, FD, emergency fund, savings account |

| Wants | 30% | Dining out, shopping, entertainment, travel |

Let us apply this to different salary levels so you can see it in real numbers:

If you earn ₹30,000/month:

- Needs (50%): ₹15,000

- Savings (20%): ₹6,000

- Wants (30%): ₹9,000

If you earn ₹50,000/month:

- Needs (50%): ₹25,000

- Savings (20%): ₹10,000 ✅

- Wants (30%): ₹15,000

If you earn ₹75,000/month:

- Needs (50%): ₹37,500

- Savings (20%): ₹15,000

- Wants (30%): ₹22,500

See how once you hit ₹50,000 per month, hitting ₹10,000 in savings becomes mathematically straightforward? And if you earn less than ₹50,000, the goal becomes to increase income while cutting wants — not to torture yourself.

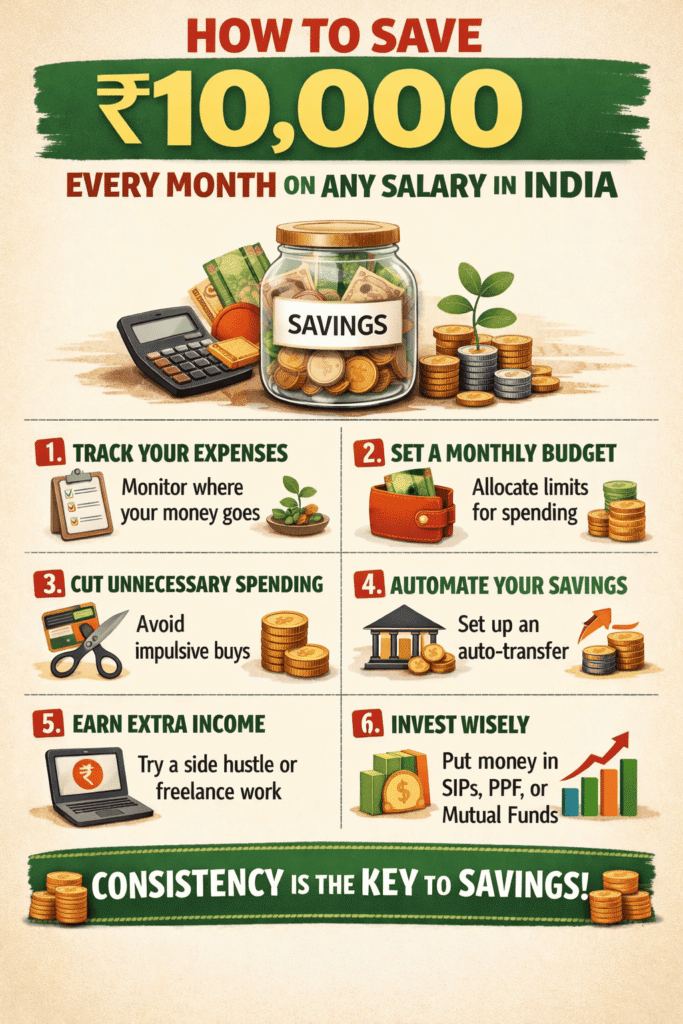

10 Real Ways to Save ₹10,000 Every Month in India

Now let us get practical. Here are 10 specific things you can do starting today.

1. Cancel Subscriptions You Forgot You Had

Pull out your bank statement right now and look at all the recurring charges. Netflix, Amazon Prime, Spotify, some app you downloaded two years ago — they all add up. The average Indian pays for 3-4 subscriptions they barely use. Cutting just two saves ₹500-800 per month.

2. Cook at Home 4 Days a Week

I am not saying never eat out. I am saying be intentional about it. If you order Swiggy or Zomato every day, you are easily spending ₹3,000-5,000 per month just on delivery fees and restaurant markup. Cook at home even 4 days a week and watch that number drop by half.

3. Use Cashback Apps and Credit Cards Smartly

If you are already spending on groceries, fuel, and bills — you might as well get paid for it. Cards like HDFC Millennia, Axis Flipkart Card, and SBI Cashback Card give 1-5% cashback on everyday spending. On ₹20,000 of monthly expenses, that is easily ₹400-1,000 back per month.

But — and this is critical — pay the full bill every month. Never pay just the minimum. Credit card interest at 36-42% per year will destroy every rupee you saved in cashback.

4. Stop Buying in EMI for Wants

EMIs are designed to make expensive things feel affordable. ₹999 per month for 24 months sounds harmless until you realise that is ₹24,000 for something you probably did not need. Before any EMI purchase, ask yourself — if I had to pay the full price today in cash, would I still buy this? If the answer is no, you do not need it.

5. Automate a SIP of Even ₹500

Here is something most people do not realise. Starting a SIP of even ₹500 per month in a mutual fund creates a habit, not just an investment. Once you see your money growing, you will want to increase the amount every few months. ₹500 becomes ₹1,000. ₹1,000 becomes ₹2,500. The habit is more valuable than the amount.

6. Build a Small Emergency Fund First

Before you invest anywhere, keep 3 months of expenses in a liquid account that you can access immediately. Why? Because without an emergency fund, every unexpected expense — a medical bill, car repair, job loss — forces you to break your investments or take a loan. Most people stay broke because they never build this buffer.

7. Do a Monthly Money Audit

Once a month — just 30 minutes — sit down and look at where every rupee went. You do not need fancy software for this. A simple spreadsheet works. Or better yet, use a pre-built budget planner that does the calculations for you automatically. When you actually see that you spent ₹4,000 on food delivery last month, it is surprisingly motivating to cut it down.

8. Negotiate Your Bills

This one feels awkward but it works. Call your internet provider, insurance company, or mobile carrier and ask if they have a better plan. You would be surprised how often they quietly offer you a discount just to keep you as a customer. Five minutes on the phone can save ₹200-500 per month.

9. Avoid Lifestyle Inflation When You Get a Raise

When your salary increases, resist the automatic urge to upgrade your lifestyle. Keep your expenses roughly the same for 3-6 months after every raise and redirect the extra income directly into savings or investments. Most people get a ₹10,000 raise and immediately spend ₹12,000 more. Do not be that person.

10. Set a Specific Goal for Your ₹10,000

Saving money without a goal is like driving without a destination — you will eventually stop. Decide exactly what you are saving for. Emergency fund? Down payment for a house? A family vacation? Your child’s education? When there is a clear, emotional reason behind the saving, it becomes much easier to say no to impulse spending.

What Does ₹10,000 Saved Every Month Actually Become?

Here is the part that should excite you. Let us look at what consistent saving actually does over time.

| Monthly Savings | Duration | At 7% Returns (FD/RD) | At 12% Returns (SIP) |

|---|---|---|---|

| ₹10,000 | 1 Year | ₹1,24,000 | ₹1,27,000 |

| ₹10,000 | 3 Years | ₹4,04,000 | ₹4,36,000 |

| ₹10,000 | 5 Years | ₹7,20,000 | ₹8,16,000 |

| ₹10,000 | 10 Years | ₹17,38,000 | ₹23,00,000 |

That ₹10,000 per month, invested consistently for 10 years at mutual fund returns, becomes ₹23 lakhs. Without any extra effort. Without any side income. Just consistent saving.

That is the power of compound interest. And the only way to unlock it is to start.

The Tool That Makes All of This Easier

I know tracking expenses manually is boring. It is also why most people stop doing it after week one.

That is exactly why I created the Creovate Official Monthly Budget Planner — a simple Excel and Google Sheets template that automatically tracks your income, categorises your expenses, and shows you exactly how much you saved each month without any manual calculations.

Everything is set up for you. Just enter your numbers. The formulas do the rest.

👉 Get the Monthly Budget Planner for just ₹149 →

FAQs — Real Questions Real People Ask

Q: I earn only ₹20,000 a month. Is it even possible to save ₹10,000? A: At ₹20,000 per month, saving ₹10,000 (50%) is very difficult unless your expenses are extremely lean. A more realistic target is ₹3,000-5,000 per month at that income level. Focus first on cutting wants, building the habit, and increasing your income through a side hustle or skill development.

Q: Where should I keep my ₹10,000 savings every month? A: Start with an emergency fund in a liquid savings account or liquid mutual fund. Once you have 3 months of expenses saved, move to a combination of SIP in equity mutual funds (for long-term growth) and FD or RD (for short-term goals).

Q: My EMIs are too high. What do I do? A: If your EMIs exceed 35% of your salary, focus first on paying off the highest interest debt — usually personal loans or credit cards. Prepay whenever you have extra money. Once EMIs come down, redirect that money straight into savings.

Q: Should I save or invest? A: Both. Saving is keeping money safe for short-term needs. Investing is growing money for long-term goals. A simple rule — save 3-6 months of expenses in a liquid account first, then invest everything else for the long term.

Q: My partner spends too much. How do I save as a couple? A: Have an honest money conversation and set shared goals. Couples who save together and track expenses together almost always make more financial progress than those who manage money separately. A shared budget planner helps enormously.

Final Thoughts — Start Small, But Start Today

Here is the truth nobody tells you. You do not need a perfect system. You do not need to read 10 finance books. You do not need to understand the stock market.

You just need to start. Today. With whatever amount you can.

Even ₹1,000 saved this month is infinitely better than ₹0. The habit matters more than the amount. Once saving becomes a habit — as automatic as brushing your teeth — the amount will naturally increase over time.

Your future self will thank you for starting today.

👉 Download the Monthly Budget Planner — ₹149 only →

This post was written based on personal experience and financial research. Always consult a certified financial advisor before making major investment decisions.